A Tale of Two Euros

Structural fractures within the Eurozone and what they mean for the Euro

As the Euro tangoes with the Dollar around the parity, it is crucial to understand a set of structural drivers behind the depreciation of the Euro as a political project. (Figure 1)

Certainly, we are in a period where things could go better for the Euro, and Europe as a whole. At the backdrop of a plethora of troubles like a persistent inflation, a deepening energy crisis, and lingering geopolitical risks from the east, we cautiously observe that the ECB has yet to demonstrate any savviness in its reading of what the markets tell. Au contraire, the recent developments in bond markets reveal once again that the ECB decision makers have no clue of the structural fractures1 within the Euro economy and what they mean for the Euro.

Fragmentation within the Eurozone

The developments of late in bond markets the ECB seems to preoccupy itself with prompted a new policy intervention that is touted as an anti-fragmentation tool. As the name suggests, this mechanism has been put on the agenda to restore a Eurozone that has been fraught with fragmentation.

To our understanding, the recent ramp-up of the Italian bond yields and the negative divergence of some troubled Eurozone economies, Italy leading, from the relatively stronger economies in the Eurozone is deemed unacceptable by the ECB — mainly on political grounds, rather than economic ones, as far as our understanding of economics goes. (Figure 2)

However, we are of the conviction that the markets, albeit laggard, have performed a separation that should be there. Whether the ECB can bear to accept it or not, the Eurozone is a structure that brings together vastly different economies, and the ECB demands that the markets treat every economy within the Eurozone as equals — which, in our view, prompts the ECB to make (repeated) mistakes.

Productivity

First off, there are severe productivity differences among Eurozone economies. Moreover, while the Eurozone is not an Optimal Currency Area due to the structural incompatibilities of the economies included, it has made the mistake of imposing on markets a common currency called the Euro.

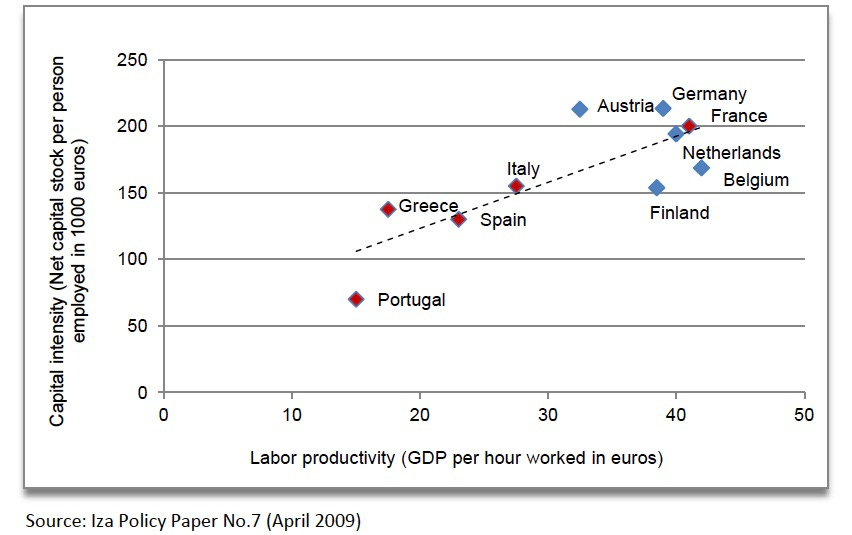

The following chart shows the differences in worker and capital productivity before the European Debt Crisis — a graph that should not be taken for granted. (Figure 3) We immediately note in the graph the divergence of two groups of economies: the more productive Northern economies clustered in the northeast, while the less productive, troubled Southern economies clustered in the southwest. To recall, the Southern Eurozone economies Portugal, Italy, Greece, and Spain were defined as PIGS with a rather pejorative acronym during the European Debt Crisis.

Surpluses and Deficits

Let us briefly touch upon the problems that a cluster of countries with such productivity differences may experience when they use the same currency, using a caricatured example:

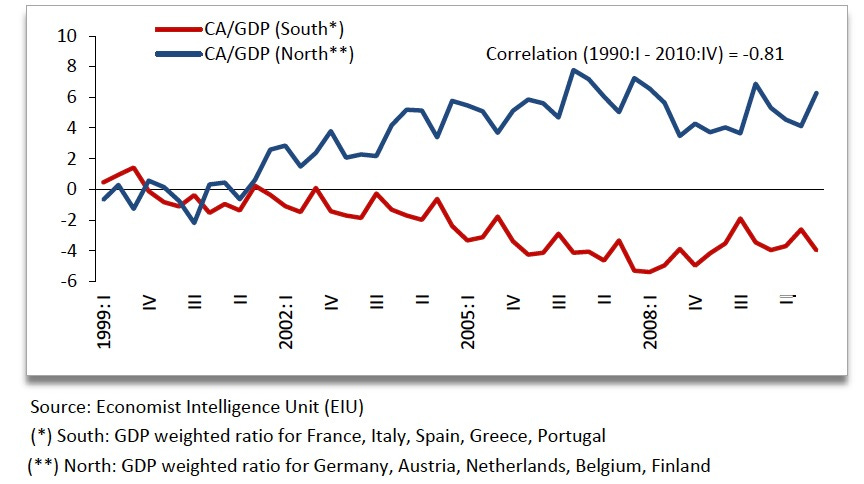

When Germany (the efficient member) and Greece (the less efficient member) switch to the same currency, that is, when the trade between them becomes foreign exchange risk–free, Greece would start to buy everything from Germany very quickly, with the cost advantage arising from the former’s productivity. It is textbook clear that Germany will end up a net exporter. As a matter of fact, since 2001, when the Euro came into circulation, we have observed this kind of sharp polarization of exporting countries against importing countries. (Figure 4)

To illustrate, imagine a Greece that is constantly buying cars from its more productive Eurozone neighbour, Germany. Despite the trade and current account surpluses that Germany would gain in this situation, a picture of Greece dealing with current account deficits that it would always have to close should come to mind.

How could the current account deficits of Greece be closed under such a structure? Naturally with the money circulating back to Greece from the German banks and other more productive members via loans issued to agents in the Greek economy.

Markets have grasped how problematic such a monetary cycle model was when the European banks stopped lending to Greece and others in PIGS, with the effect of the subprime mortgage crisis from the US. The less efficient PIGS bunch had sunk and stronger European economies such as Germany and France had to, effectively, bail them out.

In other words, it was a system where Greece bought Mercedes cars from Germany, where the Mercedes money was, in turn, pumped back into the Greek banking system via German banks. Effectively, yet another Greek citizen ended up buying a German car — say, BMW — such that both cars and money flows are always in a monetary loop between Germany and Greece.

The Call of the Yields

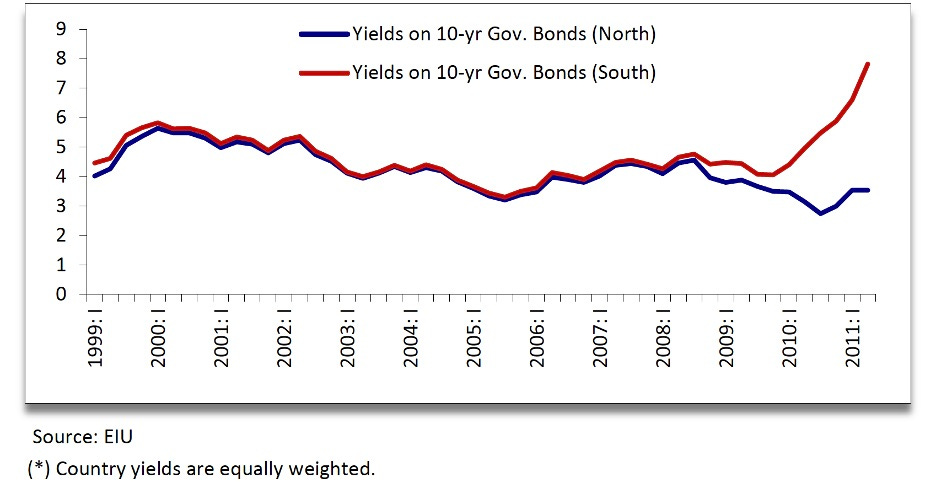

In fact, the European Debt Crisis was a clear signal that this model was neither sustainable nor viable. Hence, markets, which until then had closed their eyes to how problematic such a cycle was, sobered up and separated the better Eurozone economies from the more troubled ones for the first time in the brief history of the Euro — which is captured in the following graph. (Figure 5)

By now, markets should be well aware that the Euro is actually the fallacious currency of a problematic currency area. Further, it should be obvious that the less efficient Euro economies will always face problems if the efficient ones do not back the Euro.

In a scenario where each country used its own currency, the currency of the productive economy could appreciate, with a built-in stabilizing effect, while the currency of the less productive economy could depreciate — putting both the foreign trade and current account balances on their natural courses.

Nevertheless, this is not a possibility in such a currency union as Euro. To recall, this was one of the discussions that was heated up during the 2008–09 period. It was deliberated that Greece and other like countries should be able to leave the Euro.

The idea was that if a troubled economy like Greece returned to its own currency (the drachma), its imports would be curtailed by a depreciated drachma, while its exports would explode, and it would slowly start to earn the income that could pay its debts by its own means.

However, at that time, both France and Germany, with the very clear attitude of Sarkozy and Merkel, did not allow this lest the Euro would fail as a political currency. Moreover, the ECB did not hesitate from taking on the financial burdens of the battered Southern economies.

Same Song and Dance

Reflecting on these discussions, we are today not surprised at all given how the ECB acts. The Italian economy and its enormous debt have only grown more problematic over the past decade with its debt rising by about 45%. (Figure 6) Particularly, the current political turmoil facing the Eurozone makes it rather difficult to credibly predict the future trajectory the Italian economy could trace.

At the backdrop of all this, why is it strange that Italy’s borrowing costs diverge from those of other Eurozone economies? (Figure 7) Going back to the anti–fragmentation tool of the ECB, it is obvious that the ECB faces a bigger problem at this point.

Almost a decade ago, the then head of the ECB, Mr. Draghi famously proclaimed to “do whatever it takes to preserve the Euro.” And almost a decade later, the now head of the ECB, Ms. Lagarde has stated that a substantial divergence between the yields of the Eurozone economies cannot be tolerated.

As it turns out, the ECB will once again attempt to lower the yields of these Southern economies via a new, endless bonds purchase tool. The way we read it is, the ECB is once again rolling up its sleeves to ready for yet another brawl with the markets without the slightest consideration of how inconsistent this all is with its aspirations to slim down a gigantic balance sheet. (Figure 8)

Concluding

As the ECB descends into a renewed stand–off with the markets on how the markets should treat the Eurozone economies that have structurally different risks, concerned about a Euro we declare to be terminally diseased, we are hopeful that the reason will ultimately prevail in the markets. And prevail it always does.

In this piece, we have drawn heavily on points highlighted in Soylemez (2013).

Has this post been forwarded to you? Feel free to subscribe below:

Please note that views expressed here do not constitute investment advice. Rumelia Letters by Opes Rumelia.